The Agtech Reset - Part 2: (re)Growing Value

Why the next wave of agtech and foodtech value will be created by specialists who can both fund and fix stranded innovations.

In Part 1 of this series, we explored how a decade of misaligned capital and expectations left many ag and foodtech innovations stranded, even as fundamentals strengthened. In Part 2, we turn to the practical question: where, exactly, are the opportunities, and what does it mean to both fund and fix them. Let’s jump straight in.

Where the opportunities are

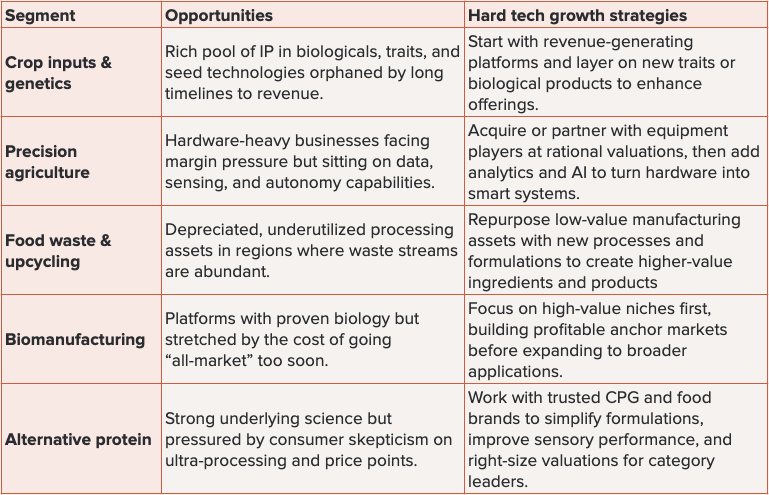

The table below summarizes a few segments where we see both stranded assets and clear strategies to unlock them:

None of these themes rely on finding the next miracle category. They rely on disciplined work: identifying real assets, aligning them with specific market needs, and connecting them to industrial partners who can help them scale.

Strategy: fix, roll up, and re-anchor

Unlocking this value is less about a single “hero” investment and more about assembling and repairing the pieces. The core moves to focus on are straightforward, although not necessarily simple:

Fix the foundation: Clean up capital structures, reset board and governance where needed, and right-size growth expectations to match the realities of regulatory timelines and industrial adoption.

Roll up adjacencies: In categories like precision agriculture, inputs, and food waste, many companies are subscale but complementary. Thoughtful consolidation can create platforms with enough product breadth and geographic coverage to matter to strategics and large customers.

Re-anchor in the value chain: The most durable businesses tend to be those that solve tangible problems for farmers, processors, and brands: yield, quality, labor, cost, resilience. Rebuilding around those jobs-to-be-done, in partnership with incumbents, can turn “nice-to-have” technologies into must-have infrastructure.

We see an opportunity to turn fragmented, underperforming innovations into scaled, credible businesses not by assuming another wave of hype, but by matching the right technologies with the right ownership, partners, and operating discipline.

Why this work belongs to hard tech specialists

Doing this well is not simply a matter of buying low. It depends on deep technical judgment, an understanding of ag and food development cycles (including regulatory), and long-standing relationships across industrial and strategic partners. The same characteristics that made some of these companies “too hard” for generic capital (the aforementioned scientific complexity, capex intensity, demanding customers) are exactly what specialists spend their careers navigating.

Pangaea, for example, has more than 25 years at the intersection of materials, chemistry, biology, and industrial markets. We have backed biological inputs for agriculture, advanced manufacturing platforms, and industrial process technologies that look and feel very similar to today’s stranded ag and foodtech assets. Often, we have done so alongside the strategics who now care deeply about inputs, resilience, and food-system transformation.

That experience does not guarantee outcomes. But it does change the kinds of questions we ask, the risks we are willing to underwrite, and the support we can provide as companies work through the messy middle between technical validation and industrial scale.

What this moment offers long-term capital partners

The combination of compressed valuations, stranded but essential technologies, and rising structural demand creates a rare scenario in ag and foodtech: more need for real solutions, fewer bidders, and assets that still matter to the food system even when sentiment is low. Fast capital and momentum trades need not apply: this is a moment for patient, technically literate investors who are prepared to fix, not just fund.

For long-term capital partners, this points to a different style of participation in the sector, grounded in careful restructuring, consolidation, and long-term partnership with operators and strategics. In our view, this is where the next wave of agtech and foodtech value will be created by doing the sustained, specialist work of bringing stranded innovations back into the heart of the food system.

This was Part 2 of our two-part Agtech Reset series. Part 1, which explores why a reset is happening and why specialists are needed, is here.